Insurance companies face catastrophic damage from climate change, yet they continue insuring and funding the biggest cause of those damages instead of preventing the “existential threat” of inaction on climate policy.

Extreme weather driven by climate change is creating record losses for insurers and their customers, and if left unchecked, those losses could triple within 30 years. But insurers are a lifeline for coal-fired power – the single largest source of greenhouse gas emissions – and without the $6 billion annual insurance market many existing coal plants would have to close while most new plants wouldn’t be built.

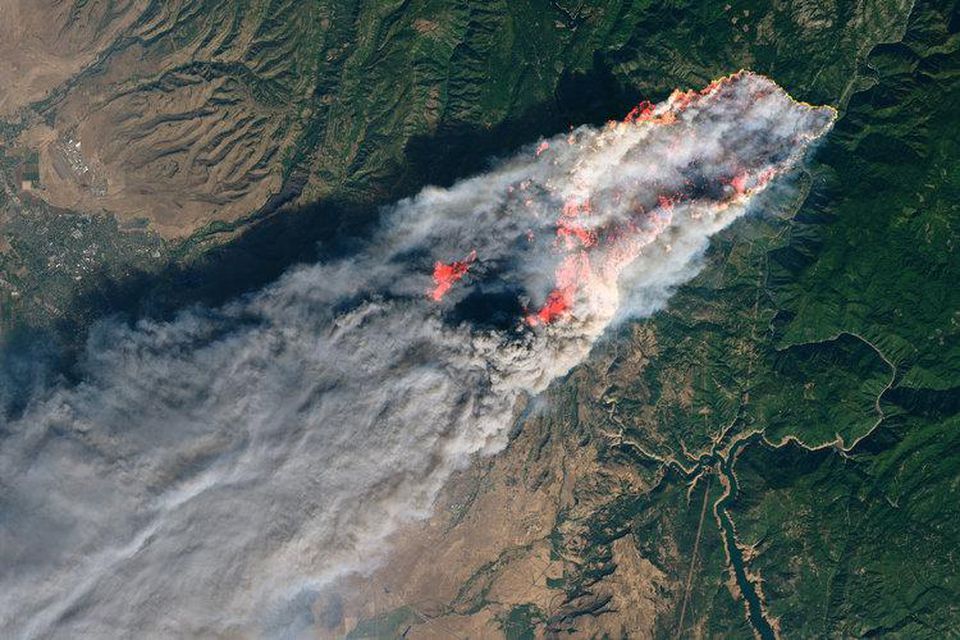

The Camp Fire, 2018’s costliest disaster for insurers by total losses, burns in California on November 8, 2018

NASA EARTH OBSERVATORY

Forward-looking insurance companies have begun waking up to this contradiction and exiting the coal industry, but U.S. insurers lag far behind the rest of the world, and how they respond could impact the global economy. As regulators consider the risks of climate change, insurance companies should shift from insuring the biggest cause of climate change to ensuring a safe climate future.

Climate change could put insurance companies out of business

Insurance companies understand the fossil fuel-climate change connection perhaps better than any other industry because they devote significant resources to assessing risk. Actuaries and climate scientists use the latest data and most advanced modeling available to calculate premium costs and decide where to offer coverage – real-life representations of climate change’s growing financial impacts.

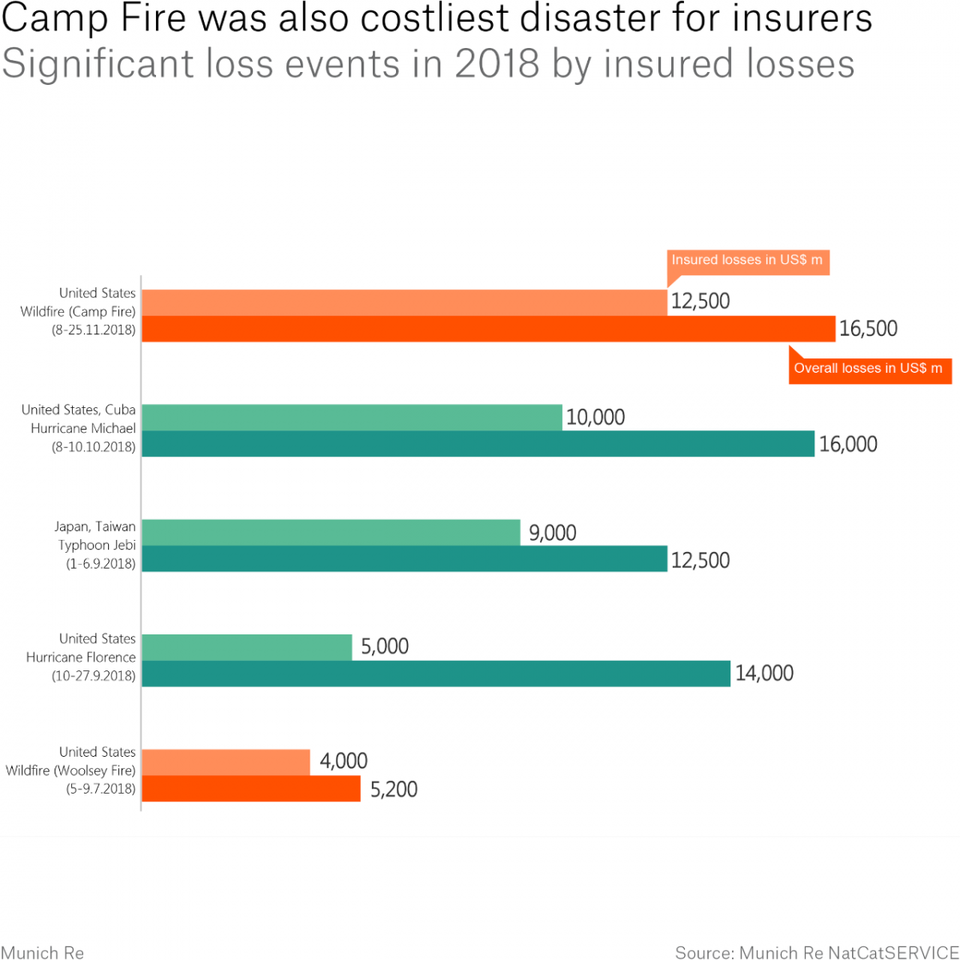

Those financial impacts set an ominous new record in 2018 with $160 billion in worldwide losses from natural disasters, paid by insurers, the individuals and businesses who suffered the losses, and the taxpayers who subsidized them through government recovery funds.

Recent research from Cambridge University predicts this trend will accelerate and warns that if climate change is left unchecked, catastrophic losses on property investments from disasters like wildfires, hurricanes, and flooding will triple over the next 30 years. In this scenario, the resulting losses to the insurance industry could cause a global financial crisis.

“A 2°C world might be insurable,” warned Henri de Castries, former Chairman and CEO of insurance giant AXA. “A 4°C world certainly would not be.”

The calculation for global insurers facing increasing climate change risks seems simple: Avoid financial ruin by preventing the worst climate change impacts. Logic would thus dictate ending coal-fired power, since it is responsible for 44% of global energy-related carbon dioxide emissions, making coal the primary contributor to climate change. Nearly 800 new coal-fired power plants are currently under construction or in the pipeline worldwide, and without insurance, most of them could not be financed or built.

Insurance companies are uniquely placed to drive the transition from coal to clean energy by ceasing to underwrite and invest in coal projects. Without their coverage of the numerous natural, technical, commercial and political risks of coal projects, new coal mines and power plants could not be built and existing operations would have to shut down.

But the insurance industry has followed a different path on coal and climate change. Global coal power insurance premiums amounted to $4.1 billion in 2017, and premiums for coal mining and transport bring the total global coal insurance market to approximately $6 billion per year.

International insurers are waking up to the climate risk – why aren’t U.S. insurers?

Insurance companies have a strong business case to stop insuring fossil fuels like coal, and many of the world’s largest insurers are responding to the challenge.

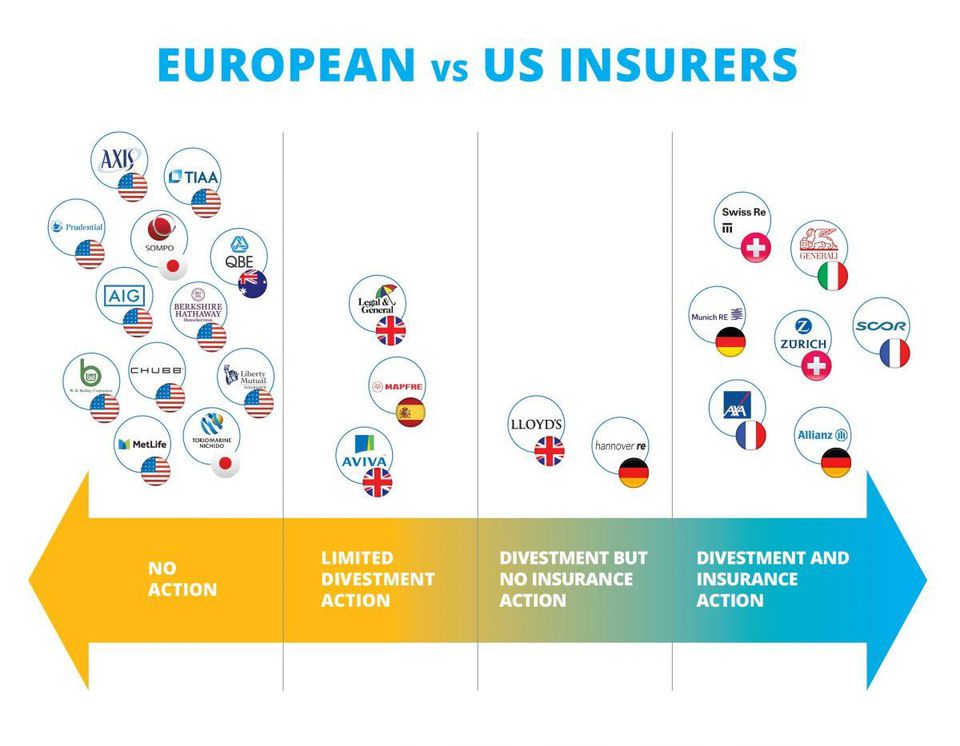

More than 20 companies, representing 20% of the insurance industry’s global assets, have exited the coal business, up from 13% a year ago. Meanwhile, 43% of the reinsurance market has now restricted coal coverage, including industry giants Swiss Re and Munich Re.

This trend is most prominent in Europe and Australia, where 22 major insurers have divested from coal and tar sands companies and 13 have stopped or limited underwriting insurance policies for the coal industry.

But United States-based insurance companies are lagging far behind their European counterparts when it comes to addressing the climate risks of insuring coal projects. No major U.S. insurance company has so far pledged to divest its holdings in fossil fuel companies or to restrict underwriting insurance for fossil fuel projects.

With many of the world’s largest insurers exiting the coal sector, U.S. insurers have an outsize role in deciding whether new coal plants are built or operated. Only a small group of insurance companies are able to conduct due diligence for power plants in Asia, where most new coal projects are proposed, and U.S. insurers are offering a lifeline to these projects by extending insurance coverage.

But the U.S. insurance industry’s financial stake in fossil fuel goes beyond insuring new coal plants and mines. The top 40 U.S. insurance companies hold more than $450 billion in coal, oil, and electric utility stock – making them more leveraged in fossil fuel than the average index fund.

By investing customer premiums in fossil fuels and enabling new coal-fired power plants, U.S. insurers are accelerating the damages they insure against and doubling down on financial risk by undermining efforts to reduce carbon emissions.

Regulation in California and abroad could drive insurer action on climate risk

The U.S. insurance industry is not required by law to disclose what fossil fuel projects it insures, or the amount of premiums it gathers from the fossil fuel industry, but regulations are beginning to change that dynamic.

In 2016, California became the first state to require insurance companies to publicly disclose their fossil fuel investments. The California Department of Insurance’s Climate Risk Carbon Initiative currently requires disclosure of fossil fuel-related investments by insurance companies writing more than $100 million in premiums. Hundreds of insurance companies have provided the information, now posted on the Department of Insurance website.

California is the largest insurance market in America and third-largest worldwide, so regulations within the state have an outsize influence on the insurance industry’s business. Since 2016 Connecticut, Minnesota, New Mexico, New York, and Washington have adopted California’s requirement – adding weight to the rule.

New regulatory oversight may soon push additional insurers away from coal, leaving U.S. insurers even more isolated in their climate risk. A division of the Bank of England responsible for conducting stress tests of the United Kingdom’s general insurance market plans to probe insurers’ climate change resilience this year.

The move is designed to focus on “cognitive dissonance in some insurers whose careful management of climate risks on the liability side of their balance sheets is not always matched by similar considerations on the asset side,” said Bank of England Governor Mark Carney.

Australian regulators have similarly signaled they will scrutinize how insurers are accounting for the economic impacts of climate change, potentially prompting insurers to act on climate risk.

Residents survey debris after Hurricane Michael hit in Mexico Beach, Florida, U.S., on Friday, Oct. 12, 2018. Search-and-rescue teams found at least one body in Mexico Beach, the ground-zero town nearly obliterated by Hurricane Michael, an official said Friday as the scale of the storm’s fury became ever clearer. Photographer: Zack Wittman/Bloomberg

© 2018 BLOOMBERG FINANCE LP

Ensuring a safe climate by not insuring coal

Insurance companies understand failing to address climate change is one of society’s biggest threats and perhaps the single largest economic risk to the industry’s own future. Yet this knowledge doesn’t determine insurers’ underwriting and investment decisions in coal-fired power, which accelerate climate change.

“Imagine a world where the same company that you purchase fire insurance from also actively insures and finances rogue teams of arsonists,” wrote Insure Our Future Senior Strategist Ross Hammond. “Ironically that’s more or less what the insurance industry is doing when it comes to climate change impacts and underwriting fossil fuel expansion.”

By failing to act, insurers face reputational and liability risks. Insurer brands depend on a reputation of protecting customers from damages, yet as public awareness of climate change impacts rise, insuring and investing in fossil fuels could become the antithesis of that brand. And analysts have established that insurers will face significant losses – perhaps the end of their industry – if the world continues burning fossil fuels and remains on its current emissions pathway.

Regulatory scrutiny is helping build the economic case against insuring fossil fuels. By getting out of the business of insuring coal-fired power, U.S. insurers and their global counterparts could invest in their own future – as well as a safe global climate.